This week, the Federal Reserve (Fed) cut the federal funds rate and the prime rate. How will this affect the mortgage rate and housing prices? How much influence does the Fed have? A lot, but that is not the whole story. There are many other facts that chime in for mortgages and housing prices.

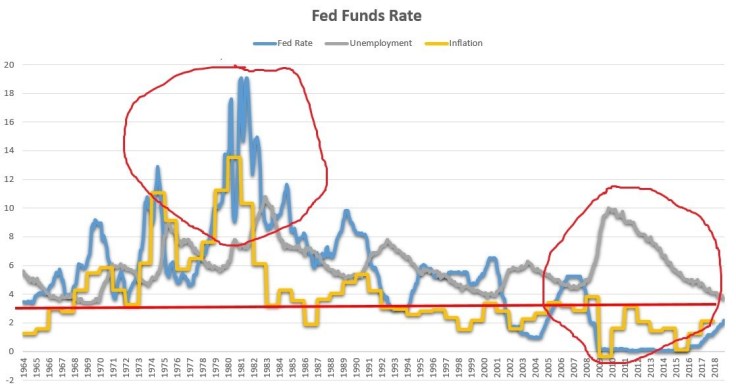

The Federal Funds Rate is 1.25% as of this writing. This is the interest rate in which Depository Institutions can borrow or lend reserves to each other when they are “temporarily” short of their required reserves. This is the base rate. The Mortgage rate is layered on top of this rate. The rest is the amount banks give to meet their market to borrow reserves from banks that have excess reserves The prime rate, is the rate that banks will extend to their most creditworthy customers which is normally 3 percentage points higher than the Federal Funds Rate. Credit Cards, for example, are layered on top of this rate.

What drives mortgage rates? Besides the Federal Funds Rate, expected inflation, economic growth or reduction prospects, and events like the Coronavirus and Government response.

Mortgage rates, which is the interest rate on a loan on a house that is given to the consumer, which is more complicated. It starts at the Federal Reserve and then the 10-year Treasury yield and Mortgage Bonds that together determine the rate banks get their money. Then that is layered on top is the lenders pricing models which is in competition with other lenders that also helps keep it down. So, the Fed lends money at near 0%, then the Bank may charge 3.25 to 4% to cover the cost of the loan and a profit margin. This is depends also on the credit rating of the customer and the amount, length and the terms of the loan. https://www.bankrate.com/

When the Federal Reserve increases or lowers its rates such as by lowering the short-term discount rate this triggers the rest of the economic cycle and mortgage costs. As investors will be in a frenzy to buy or sell off mortgage-backed securities motivated by greed or fear. Thus, in response to the insecurity of the Coronavirus and the impact on the economy, the Fed has cut the Fed Funds Rate down to 1.50% to simulate the economy and try to ward off a Recession. This is also fueled by fake news online, and irresponsible fear reporting by the media, which is scaring off investors and confusing consumers. Which is why the stock market has been on a roller coaster. Because the rates are already at rock bottom, the actual mortgage rates may not be affected. But, this may cause consumers to buy a house or refinance a loan. Which has a great impact on the rest of the economy.

In other good news, because of the lower Federal Funds Rate, some of the lending rates at banks will positively affect short-term loans like auto and home equity lines of credit. However, your CD and savings deposit rate will most likely go down too. Time will tell if Credit Cards will be affected.

The next big economic factor will be how the housing market reacts. What determines housing prices? It is all about supply and demand from six main components, location, rent prices, available housing units, the cost of current inventory, the availability of borrowing, and prospects of future price changes. Why houses are more expensive in San Francisco, desirability, little availability and location, and cheap in Visalia, an undesirability (although I liked living there), a lot of inventory and location. In addition, the local tax assessor also uses the above factors to determine the estimated market values and thus the property tax of all the properties in their community.

The good news is the Government is using whatever tools they can muster to help the U.S. economy. And remember, the Coronavirus is just passing through. It will burn itself out fueling a full recovery. The best case, before the Elections in November. The worst case, like the recovery from 1987 took two years and after the drop in 2008 it took six years.

https://www.federalreserve.gov/faqs/credit_12846.htm

https://www.cnbc.com/2019/09/18/heres-what-the-feds-interest-rate-cut-means-for-your-wallet.html

If you are in Southern California, my firm can help your family and business. Let me know; I can show you how to invest safe, biblically and prepare for your future… And, we are hiring!

Leave a comment