Are Annuities Bad for Retirement?

There is a common objection about Annuities; I would like to clear up. It goes like this: “Annuities are terrible because when you die, the insurance company will stop the payments and they will keep the rest of your money.” Is this true or false?

Many securities people do not like annuities and will talk their people out of them for many reasons, especially with the above objection. In addition, they are not properly licensed or trained to deal with them. They are qualified only to know and like products that are variable. They do not like products that do not lose money, as it is seen as unfair competition. They love the risk and the high of gambling, and annuities are safe. In addition, they are captive to their company that do not offer them, and they need to focus on their quotas. I know because I was one of them for many years.

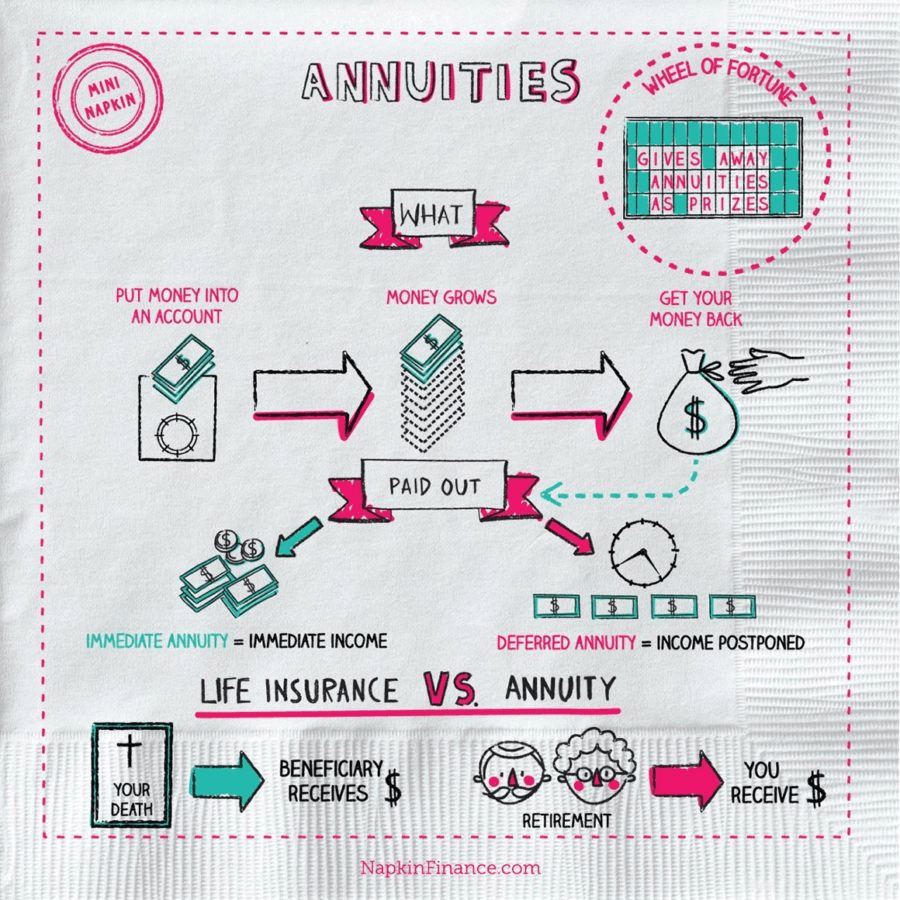

First off, what is an annuity? An Annuity is a contract with an insurance company. That is it.

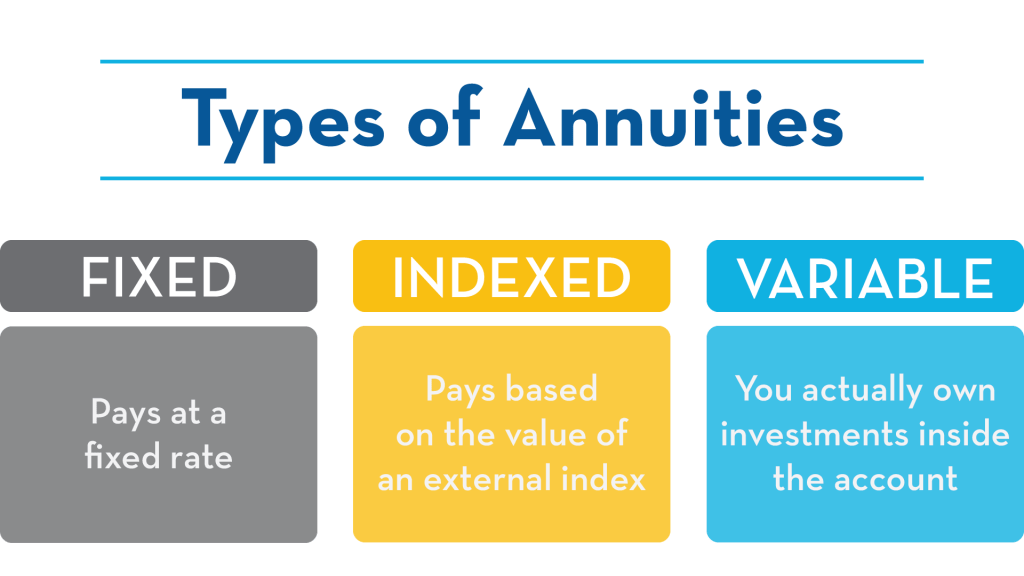

An annuity contract is when you make a lump-sum payment or series of payments and, in return, receive regular disbursements. Such as a series of payments made at equal intervals after a period of growth or at any time stipulated. This is a long-term investment that has significant tax-advantages, like tax-free growth. They can provide a safe steady income resource during your retirement. Thus, an annuity can be written the way the objection implies, or anyway, depending on the circumstances. By the way, that is how most pensions work. However, an annuity can also be written so the payments can still be paid out until the money is exhausted to a beneficiary. It is all about how the terms and conditions are written. As with all contracts, all are different and individualized to the needs of the parties involved.

The bottom line is, no, not all annuities are bad, just like not all contracts are bad. Some are good and some are bad. It is all about how they are written!

The contract has terms and conditions and is a promise of the who, the parties involved, the amount the time, and distribution involved. The insurance company or bank cannot keep your money unless it is contracted to do so. And if it were to keep your money outside of the terms, that will be illegal, and the SEC and other regulatory departments will go after them and you will have a juicy lawsuit.

Years ago, some annuities were written that way to annualized like a pension in the manner of the objection. How annuities work now is much more beneficial to the annuitant (who is the investor) and the beneficiary (who is entitled to receive the payments) of a retirement or other fund. For example, if you put a hundred thousand dollars in and it grows, then when you are ready to retire, that money plus its accumulated growth value is cut up and annualized over the specified amount and period of time. Usually, to when the money runs out.

So, the real problem is, if you live too short or too long. With a pension if you live too short, there is usually only a funeral payout and the rest of the fund reverts back to the company that holds the pension. If you live too long, a pension may still cover you. However, with an annuity, the cash value and accumulated value may run out and then you are not covered. That is the case with most older annuities. The solution is, some newer annuities have a lifetime payout, even when the money runs out, like a pension. Some companies give 10-20% bonus and compounded interest rates of 7-12+%. While most 401 (k)’s are 4-8% with excess fees and large loss rates.

Annuities can be the best plan for retirement. You can rollover old 401 (k)’s or IRA’s into them for a higher growth rate, a significant reduction in fees, tax free growth, and without any fear of loss.

You need to talk to a licensed professional who is specialized in annuities to help you get the right company and the right plan for your best benefit. We can do that for you!

Dr. Richard Krejcir is a licensed and experienced Financial Consultant with over thirty years of experience. He has worked for major banks, insurance companies, nonprofits, and families too. He is also an author, pastor, Special Ed Teacher, and financial blogger and holds a doctorate in Stewardship.

Leave a comment