Note: This article will be updated as new information is made available.

The law starts in three stages. First, June 30, 2020, for companies with more than 100 employees. Then, on June 30, 2021, for businesses with more than 50 employees. The third stage will go into effect on June 30, 2022, for employers who have five or more employees.

First off, there is a massive retirement savings crisis looming on the horizon and our Government is expecting small business owners to solve the problem with State-mandated retirement plans!

The businesses that will be affected are those with five or more employees that do not already offer a retirement plan in place for their employees.

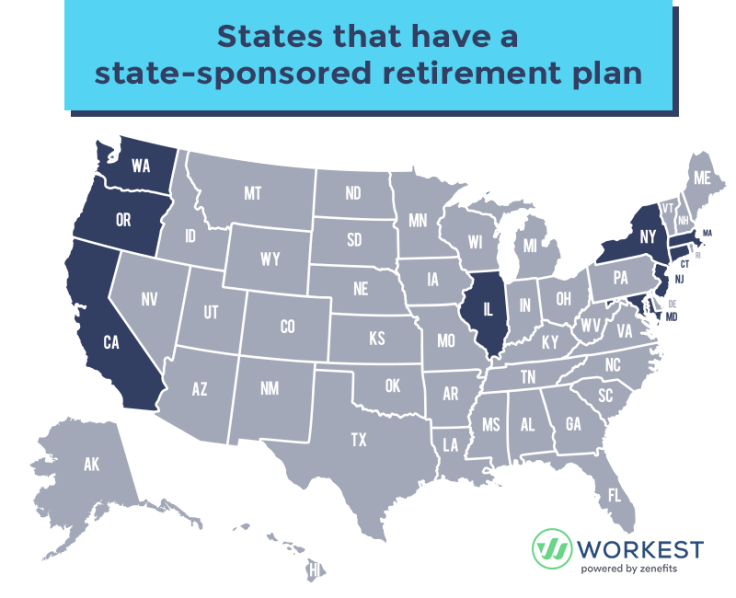

The States that are affected are: California, Connecticut, Illinois, Maryland, Massachusetts, New Jersey, New York, Oregon, Vermont, Washington with other States considering it.

The State solution is to create an exchange and or State sponsored IRA, individual retirement accounts. Similar to what the ‘unaffordable’ health care act did. And, we know how well that worked out for our health care system. The goal is to have a Roth IRA (after-tax money that grows tax free) for each worker. While employers will have to take out a 3%-5% payroll deduction.

The Positive Implications

- The reasoning for this program is good, because most 401k programs are not working, and Social Security may not be around. So, this is a way for employees to save for their retirement.

- The AARP believes workers will be more likely to contribute to a plan that is State sponsored. And, the typical worker will not create their own retirement plans.

- Research shows when the funds are withdrawn from the paycheck instead of afterwards workers are more likely to contribute.

- Employers may not have to pay for the State-sponsored IRA plans, which will be fairly basic without any workable options.

- A business may not have fiduciary responsibility (be a legal representative) for the plan.

- There are legal challenges underway, as these State IRA plans are firmly opposed by those in the financial services’ industry.

Some Notable Objections

- Small business owners will be obligated to distribute State-supplied plan information and enroll their workers.

- Small businesses pay significantly more for traditional 401(k) retirement plans than larger companies do. Thus, this will not be affordable.

- Most Employers stay away from 401(k) plans, because they are too costly and complex. Larger companies have departments that manage them alongside the financial firms that hold them.

- Employers will have to act as the brokers and agents for the employees, which few will know how and what to do.

- Although the State will give workers the IRA information, it will not be understandable or easy to follow.

- The State may automatically enroll small business workers in the State plans without any warning.

- This will put an unnecessary burden on small businesses, forcing them to comply with the mandatory programs.

- This Act may violate the Labor Department’s “safe harbor” rules.

- As with all government programs, the plans will be risky, mismanaged, and expensive.

- Small business owners may have to violate SEC, Securities and Exchange Commission’s rules and act as a financial adviser for their workers and placing them in serious legal jeopardy with other State and Federal Regulatory agencies.

When have you ever been a part of a government program that actually worked well? Where there was smooth, competent leadership, careful planning, your best interests in mind and actual productive growth? So, do you want the State to control you and your employee’s retirement where it will most likely be mishandled and lose, or an A+ company that has been around for 150 years that has guaranteed growth?

We have licensed fiduciary experts who can cut through all the red tape, get you and your employees the best plans from the best A+ companies in A grade mutual funds (typical 401k’s are in D grade) for the best price and we will actually watch over them to evaluate market losses! No one else will actually do that for you!

https://humaninterest.com/blog/small-business-owners-required-to-offer-retirement-plans-under-new-state-laws/

https://www.wsj.com/articles/states-take-aim-at-people-with-no-retirement-plan-11593945474

https://employer.calsavers.com/home/employers/program-details.html

https://humaninterest.com/blog/what-you-need-to-know-about-the-retirement-crisis/

https://www.aarp.org/content/dam/aarp/ppi/2014-10/aarp-workplace-retirement-plans-build-economic-security.pdf

https://www.barrons.com/articles/no-401-k-retirement-plan-at-work-some-states-want-to-help-51580387402

https://www.sba.gov/content/small-business-retirement-plan-availability-and-worker-participation

https://connecteam.com/state-mandated-retirement-plan/#:~:text=A%20state%2Dmandated%20retirement%20plan,systems%20for%20public%20sector%20employees.

For help with insurance, business plans, debt management, and rolling over 401k’s to a secure high yielding retirement fund with tax advantages, that will not lose your money, give us a shout, we are here to help you. seminarsonmoney@gmail.com

Dr. Richard Krejcir is a licensed and experienced Financial Consultant with over thirty years of experience. He has worked for major banks, insurance companies, nonprofits, and families too. He is also an author, pastor, Special Ed Teacher, and financial blogger and holds a doctorate in Stewardship.

Leave a comment