An IRA is an Individual Retirement Account. It is basically a retirement plan that allows you to save money for retirement with a tax advantage. This is a service provided by banks and various financial institutions as well as Insurance Companies that will manage your retirement savings. Depending on the type and how it is set up, it usually has tax-free growth or has a tax-deferred basis. You pay the tax before the money goes in or after it comes out. Versus a retirement savings account where you pay the tax going on, while it is in there, and when you take it out, just like a regular savings account. Which is why IRA’s are preferred and why they have replaced pensions.

The main types of Individual Retirement Account are: The Traditional IRA, and the Roth IRA. Then there are, SEP IRA, Nondeductible IRA, Spousal IRA, SIMPLE IRA, and the Self-directed IRA.

There are Two Types of Qualified Tax Retirement Accounts

First, is a Qualified Retirement Plan, it is recognized by the IRS as a retirement investment in which the income accumulates at a tax-deferred rate, so tax-deferred contributions are from the employee. In addition, the employer may also deduct amounts they contribute to the plan. Examples are most work-based IRA’s, individual retirement accounts that are “sponsored” through your employer, such as, 401 (k), pension plans and Keogh plans.

Second, is a Non-Qualified Plan, which is a non-deductible IRA, these are just retirement savings plans. So, you cannot deduct contributions from your income taxes as you would with a traditional IRA. They are called non-qualified because they are not from an employer and thus are qualified from ERISA guidelines (Employee Retirement Income Security Act). These plans are usually used for higher paid executives whose income is above the IRS rules for IRA’s. They use after-tax dollars to fund the plan and, usually the employer cannot claim their contributions as a tax deduction.

The Types of Retirement Accounts

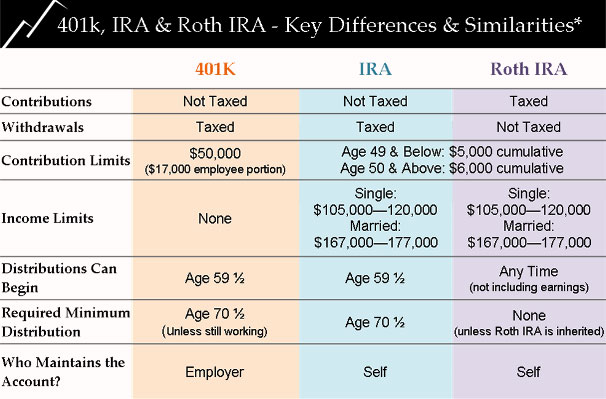

A Traditional IRA is an individual retirement sometimes set up as a 401(k) account usually has tax advantages to reduce your tax bill today. There is usually a tax deduction for money that is set aside for retirement. The investment earnings on those contributions are not taxed until they are withdrawn. Anyone can contribute to a traditional IRA, but not everyone can deduct contributions. These are usually “qualified” retirement because they are offered through an employer. Only employers are is allowed to “sponsor” a 401k for their employees.

A 401(k) plan is the tax-qualified, contribution pension account defined in subsection 401 (k) of the Internal Revenue Code.

A Roth 401(k) is an employer-sponsored investment savings account that is funded with after-tax dollars up to the plan’s contribution limit. This means you pay the tax going in and the withdrawals in retirement are tax-free. The difference with a traditional IRA you will have to pay taxes on the amount you withdraw based on your current tax rate at the time of retirement. This type of IRA is good for people who will be in a higher tax bracket in retirement than they are now, as withdrawals are tax free.

A Simplified Employee Pension (SEP) IRA is a retirement savings plan offered by employers and self-employed people that benefits their employees and themselves. Employers may make tax-deductible contributions on behalf of eligible employees.

A Spousal IRA is a retirement strategy that allows a working spouse to contribute to an individual retirement account.

A SIMPLE IRA (savings incentive match for employees) is an employer-sponsored retirement plan offered within small businesses with 100 or fewer employees. They are usually less expensive and less complicated alternative to traditional 401 (k) plan.

A Self-Directed IRA (SDIRA) is an Individual Retirement Account that allows you to have greater control and diversification. Unlike other IRA’s, you are not limited to stocks, bonds, or mutual funds.

IRA’s have a “TPA,” this is the Third Party Administrator. This is usually the organization that manages many day-to-day running of your employee retirement plan. A TPA administrator files the IRS 550 forms yearly. There other responsibilities include the retirement plan documents and preparing the employer and employee statements.

How is Your IRA Doing?

You can check your 401(k) at this website www.brightscope.com and see how it is performing and all the stats. You will be shocked that there are very few, if any, good plans, some of the best companies have their employees on ones that are at around 50, which is an F and the best ones are at 80, a low B on a grade scale. You can also go here finance.yahoo.com to see how the various plans in your 401(k) have performed over the years. Most lose more money than what they gain, money that you have is put in is leaking out. You can do better, we can help!

Limits and Downsides

The annual limit for a ROTH IRA is $6,000 for those under 50. If you are over 50, then the limit is $7,000 a year. At 59 1/2 you can take your money out. There are income limitations. If you make too much money, $280,000 or more a year, then you can’t have one (check current IRS rules).

The maximum amount you can contribute to a 401 (k) usually changes each year based on IRS regulations. For 2019, the contribution limits for 401 (k) plans are $19,000 for employees under 50 and $25,000 for those over 50.

The Downsides to not having an IRA and 401 K is there is usually no company matching funds. Although, the growth rate is usually less than the loss rate. Keep in mind that company retirement plans typically benefit the company, not the employee.

There are better choices out there, like an IUL (We will discuss in the next article). So, if you have an old IRA from a previous employer, why keep it there. You will have less interest, usually fees and it is not properly managed. It’s like staying with an ex-relationship when you have moved on. So, roll it over! We can show you how and with a company that will not lose your money, no losses!

What Happens to an IRA after you Leave an Employer?

When you leave a job, you have the right to move “your” money from your former employer sponsored IRA without paying any income taxes on it, which you should do as soon as possible. As long as it is moved to a properly qualified account. You can use any financial institution or Insurance Company that you choose. However, we know the best companies that you can do better with.

They let you go, are taking your 401k / IRA with you? Why would you leave your money there? Why don’t you take your money with you?

99 times out of a hundred, there are far better plans out there.

Rollover 1035, allows you to take bigger sums into the account that is not limited to income or annual amounts. Remember, it is your account, it does not belong to a corporation or financial firm. Better to have no fees and can grow your retirement further and faster and better with an index strategy.

You can usually only rollover and old 401 k, a company you used to work for. Current employers usually do not allow you to take them out as they use that money for their balance sheets, even though it is not their money. Although, some companies will allow you to, so check with your HR department.

There are better plans out there! The vast majority of 401(k)’s are designed to benefit the company, not the employee. That is another reason why companies dumped pensions for IRA’s.

The IRA was not designed to replace a pension or a personal retirement plan. When they were first stated in the 70’s it was part of a “Three Legged Stool,” of Pension, Social Security and a 401(k).

Many Financial Advisors who are captive to one firm may not even know about them. They will only sell you what they get the best commission on or what they are told to sell, not always what is best for you. These plans, such as certain annuities and even life insurance. Because plans like an Index Strategy have even better tax advantages and growth rates than what your employer offers or what you have sitting in a forgotten account.

We can help you with that!

Check all of the above with current IRS rules.

https://www.irs.gov/retirement-plans/401k-plans

https://www.irs.gov/retirement-plans/roth-acct-in-your-retirement-plan

Allow us and the independent brokerage houses we work with to help you. We have over 300 companies we work with, and we can search to find the best possible solution for you, your business and family. We will work for you, not any company.

Leave a comment