The question is, what have been some of the best-performing investments over the last seventy-plus years? What have been the safest ways to invest in that same period, if structured properly, even in market chaos? Where do the top 1% of income earners place their significant portfolio in? The answer, as the top financial analysts say, it is Index Funds!

What is an Index Fund

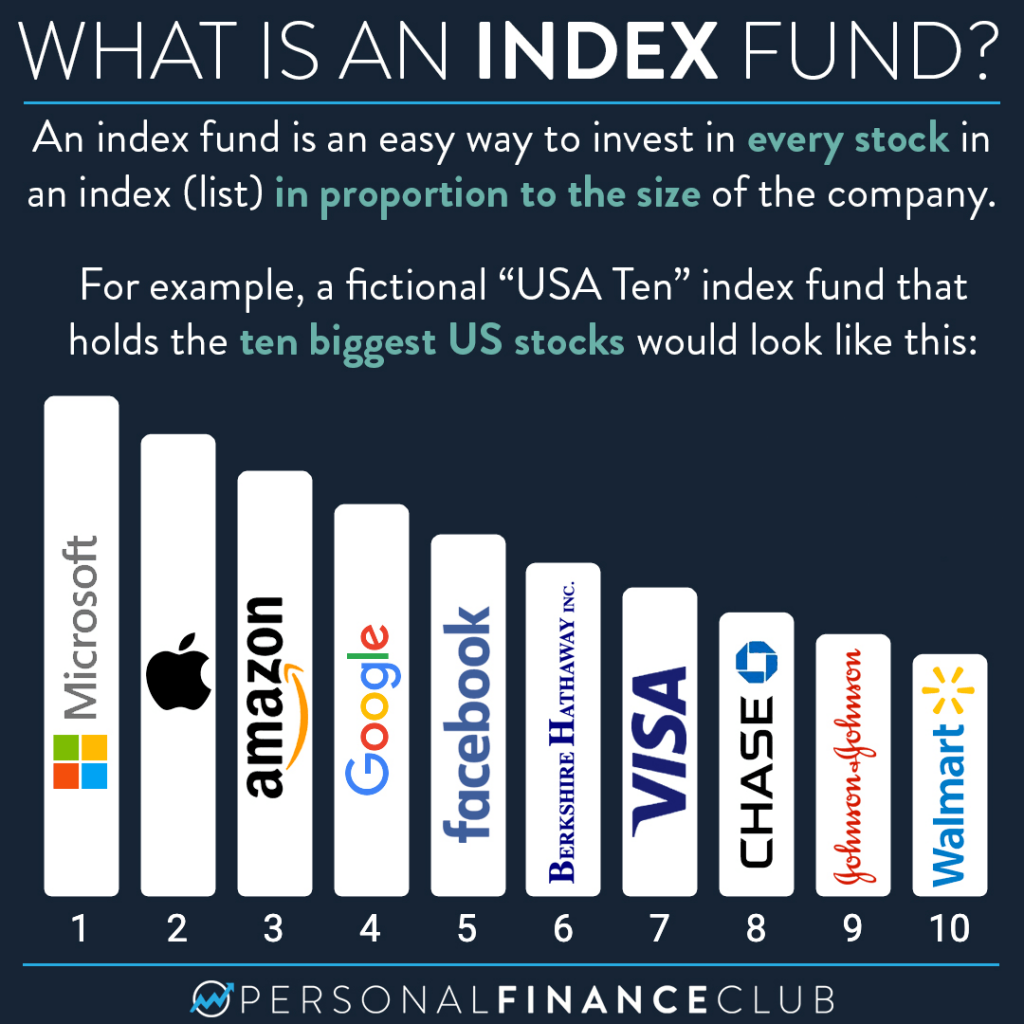

Principally, an index fund is an exchange-traded portfolio of stocks and bonds designed to follow certain preset rules or the performance of a financial market. Similar to a structured group of stocks in some mutual funds.

For example, the S&P 500 is made from the top 500 publicly traded companies in the United States. Most financial experts agree that a well-diversified portfolio such as some buy-and-hold mutual funds are very good investments, especially for long-term investors. Additionally, they are low-cost to get into and maintain and require little personal management, or worry about the ups and downs of the market. As they performed remarkably, compared to traditional mutual and investment funds in the last seventy-plus years, including in 1987, 2000, 2008, and 2020.

Here is where we venture into the weeds and then the forest a bit. There are over 5,000 index funds from the S&P 500, Nasdaq 100, the original Dow Jones Industrial Average (the company that publishes the Wall Street Journal), and so forth. So many funds are willing to take your money. One of the first was from Thomas Edison who founded General Electric. The S&P 500 is a favorite of many which includes Apple, Caterpillar, Coke a Cola, Microsoft, Procter & Gamble, and well, 495 more. Keep in mind that this fund is made up of the 500 top-growing companies in the United States. They are usually part of every good mutual fund and 401k and investment portfolio. The rest of the 5000 plus funds, well, there are some great ones and mostly mediocre and some very bad ones.

Unfortunately, many times a good Index Fund is usually only a small portion of your retirement account, the part that grows and you do not lose over time.

What are Index Funds Made of?

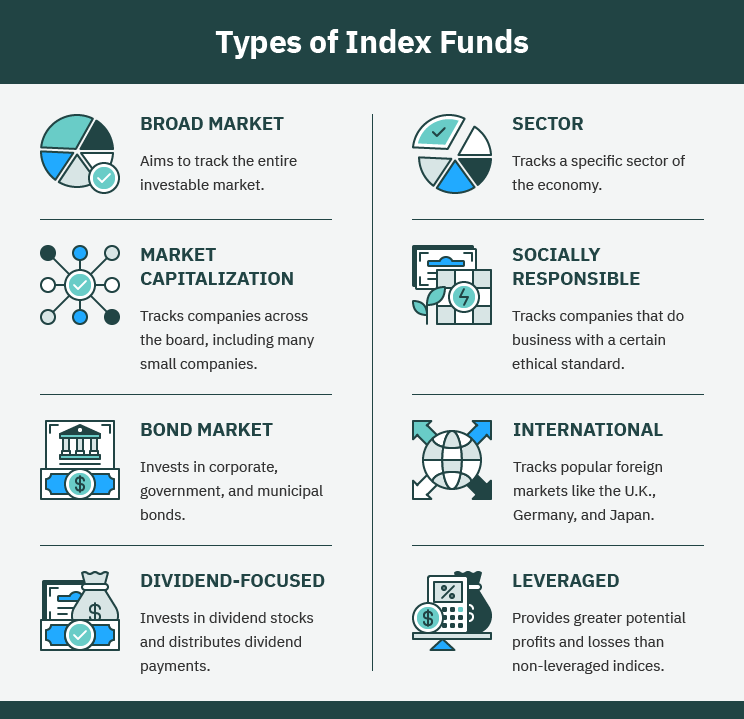

They are either a portfolio of housed stocks and Bonds, or an investment fund that follows a benchmark index, such as the Nasdaq 100. When you put money in an index fund, that cash is then used to invest in all the companies that make up the particular index, which gives you a more diverse portfolio than if you were buying individual stocks. So, which one to pick? That is what we do, we are on top of it. Good luck without a fiduciary who has your back.

Imagine going into a casino and knowing that there are slot machines and tables that will not lose and even give good payouts. But a few will break even, and most will lose your money. Which ones to go to the trick.

Here is the danger, if you are not savvy and do not know the future if one sock is better than another, it is much safer to bet a spread in the top 100 or 500 best-performing companies. If you bet on the wrong companies, then you could lose it all. Yes, I am using gambling language for a reason (I am not a gambler.), no one knows the future. We just look at the health of the companies, their outlook, and their stats. The spread works because most companies will do great which equalizes the odds. And the ones that the ones that are sound. does not offset This is why diversification is so important.

It is best to use an index fund as a strategy to build an income base to draw a dividend check for life. Or even better, place it into a tax shelter with safeguards that guarantees you will never lose your money!

Which Index Funds are Best?

Some of the better Index Funds are the S&P with a point-to-point, where you gain from the average of a 12-month range. Which would have saved you big in 2008 and 2020! Sometimes these are capped at 12%, but they have a 0, which is a Zero floor. That means your money never goes down. All the upside of a market with no downside. Sometimes the financial institution will charge a rate increase or rate fee, to bring you past the cap. Your money is safe, protected, and growing!

There are S&P Indexes with monthly averages with a cap of 2.5% and others with very low participation rates. Remember that is why you need a seasoned financial professional who is not captive to any one company and therefore can look at a hundred companies and find the right one for your situation. We can run the numbers and find the best one for you. Like the Balance Global index with a 200% – 250% participation rate, that means it is earning if the market goes up 10%, you get 20%. This is done by buying options and a venture into calculus derivatives. Good thing I teach math too.

To get more into the weeds, the US Fundamental Ballance Index, is a domestic group of stocks and bonds with a rate booster that sometimes has a 200% participation rate. And others that mimic that which do not perform well. This can get very complicated and convoluted and most licensed stock guys do not know how they work or even that they exist.

Why Does My Financial Adviser Not Know About This?

Usually, they are not licensed for it or have been told they are bad because they are not offered by their firm. Why? The commissions are much bigger in securities. Also, they make money from your loss. Most brokerages and their licensed employees only go off what their company is pushing that gives them the best positions. Many times, their funds are junk funds and indexes mixed. I know this because I worked in that industry for many years.

We do not do that. We have people who know exactly how this work. Like me with a PhD in finance who studies this and only gives you the best options for you, not what is best for us; rather, what works best for you!

So many funds are willing to take your money. Let us help you choose and save and protect your money!

Make sure your money is working and growing for you!

Dr. Richard Krejcir is a pastor, teacher, and a licensed and experienced Financial Consultant with over thirty years of experience. He has worked for major banks, insurance companies, nonprofits, and families too. He is also an author, Special Ed Teacher, and financial blogger and holds a doctorate in Finance and Stewardship.

Leave a comment