As of May 20, 2020, there is still funds available. First, go to your business bank and see how they can help you.

Update as of April 24, 2020

- A new $484 billion coronavirus relief package has been signed on Thursday, April 23, 2020.

- The new bill contains about $320 billion for the Paycheck Protection Program (PPP) and $60 billion for the SBA’s Economic Injury Disaster Loan (EIDL) program. It’s also providing about $75 billion for hospitals and $25 billion for coronavirus testing.

- EIDL and PPP loans are processed on a first-come, first-served basis.

- The $360 billion funding from the first bill has depleted within two weeks since it opened last March 27, 2020.

- Lawmakers are still expected to put together a larger package to follow the CARES Act.

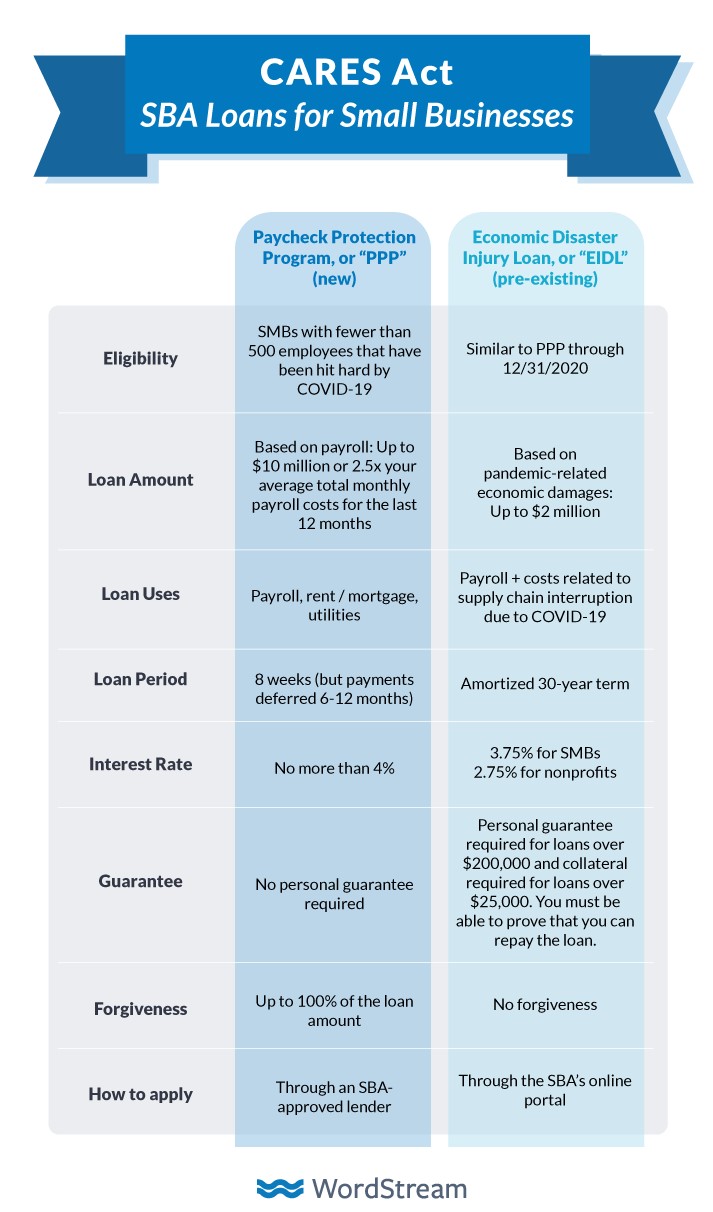

On March 27, 2020, the largest economic recovery package in American history has been signed into law. The Coronavirus Aid, Relief, and Economic Security (CARES) Act of 2020 will allocate $350 billion for small businesses affected by the pandemic through loan programs: an expanded Economic Injury Disaster Loan (EIDL) program and the Paycheck Protection Program (PPP).

The PPP loans aim to provide the liquidity that small businesses need to support employees during the pandemic.

The EIDL program will help small businesses recover for broader economic injury related to the outbreak. Borrowers can request a cash grant of $10,000 which will be released 3 days after their application. The advanced funds do not need to be returned in the event the EIDL is denied.

First, check with your business bank before going to the SBA, below is last resort:

Our table can help you determine which Small Business Administration (SBA) loan will fit your business needs.

| Paycheck Protection Program (PPP) | Economic Injury Disaster Loan (EIDL) | |

|---|---|---|

| Loan Period | February 15, 2020 to June 30, 2020 | January 31, 2020 to December 31, 2020 |

| Loan Term | Up to 2 years for the unforgiven portion of the loan indicated by the SBA | Up to 30 years |

| Maximum Loan Amount | $10 million | $2 million |

| Interest | Not to exceed 1% | Not to exceed 3.75% for businesses Not to exceed 2.75% for non-profits |

| Eligible Borrowers |

|

|

| Loan Usage | Payroll except for compensation in excess of $100,000, mortgage interest, rent, utility expenses, and pre-existing loans. | Fixed debts, payroll, working capital, inventory, accounts payable, rent, utilities and other operating expenses that cannot be paid because of the disaster’s impact. |

| Application Process | Apply through SBA-approved banks and lenders. | Apply directly through SBA’s website. |

| Debt Forgiveness | Loan forgiveness may be applied to 8 weeks’ worth of funds allocated for payroll cost, mortgage interest, rent, and utility expenses incurred after receiving funding.

The forgiven amount may be reduced in proportion to any employee or payroll reduction during the 8-week period. employees or 25% reduction in payroll on June 30, 2020 compared to pre-February 15, 2020 levels. |

Loan forgiveness may only be applied to the $10,000 emergency cash grant.,The cash grants will also be credited towards the maximum forgivable amount under any PPP loan. |

| Personal Guarantee | No required personal guarantee | No required personal guarantee for loans below $200,000. |

| Collateral | No collateral required | Collateral may be required for loans exceeding $25,000 |

Here are some of the most pressing questions and answers about these loans:

Q:

Q:

A:

- Businesses, nonprofit, and veterans service organizations with less than 500 employees, with certain exceptions; and – were operational as of January 30, 2020 (for EIDL) and February 15, 2020 or earlier (for PPP) – can show proof of payment for employee salaries, payroll taxes, or independent contractor fees.

- Businesses in the food and hospitality industry with more than one location who employ less than 500 employees per location.

- Self-employed and gig workers, including ride-sharing company drivers.

- The 500-employee threshold includes all statuses: full-time, part-time, etc.

Q:

Q:

Paycheck Protection Program (PPP)

Q:

A:

- Through banks, credit unions, and private lenders approved to issue 7(a) small business loans.

- You can apply to more than 1,800 SBA 7(a) banks.

- There are plans from the Treasury Department to roll out new regulations that will make it possible for almost all FDIC-insured banks to release SBA loans.

- Loan applications may be processed beginning April 3, 2020.

Q:

A:

- Borrowers are advised to prepare documentation of their business operating expenses and revenue.

- PPP loans will require the accomplished application form and may require other documentation for business eligibility.

Q:

A:

- PPP loans are intended to encourage businesses to rehire and keep employees by paying allowable payroll costs, costs related to the continuation of group healthcare benefits during periods of paid sick, medical or family leave, insurance premiums, interest on mortgage obligations (but not principal payments), rent (including utilities), interest on debt incurred before February 15, 2020. Additionally, the SBA has indicated that at least 75% of the forgiven amount needs to be spent on payroll costs only. The loan proceeds may not be used to pay salaries over US$100,000.

- If you are applying for both PPP and EIDL loans, each should be used to cover different expenses.

Q:

A:

- PPP loan borrowers can receive maximum of $10 million.

- For PPP, lenders are instructed to use a formula that takes into account how much the business previously spent on payroll expenses to determine the appropriate loan amount

- PPP borrowers can receive up to 2.5 times the average monthly payroll for 12 months before the date the loan is made. For seasonal business, you can receive up to 2.5 the average total monthly payments for payroll costs starting Feb. 15, 2019 or March 1, 2019 (decided by the loan recipient) and ending June 30, 2019. Compensation exceeding $100,000, payroll and income taxes are excluded.

Q:

Q:

Q:

A:

- PPP loan forgiveness is offered for businesses that retain employees or rehire those that had been laid off during the outbreak. Loan forgiveness can be applied to portions of the loan spent on payroll, rent payment, utilities, and mortgage expenses incurred within an 8-week period since the start of the loan’s origination date.

- Loan forgiveness for PPP will be reduced if borrowers reduce their number of employees and decrease salaries and wages by more than 25% for any employee.

- Businesses with PPP loans have until June 30, 2020 to reinstate employee numbers or salaries that changed between Feb. 15, 2020 and April 26, 2020 and maintain eligibility for loan forgiveness

Q:

Economic Injury Disaster Loan (EIDL)

Q:

A:

- EIDL borrowers are advised to prepare documents and certification that they need the loan for business-related payments (e.g. payroll, lease, utilities) during this economic uncertainty.

- Small-business owners can apply directly on the SBA website. You can submit your application and indicate if you wish to receive the emergency grant of $10,000.

- You should be able to receive the grant within three (3) days if your application.

Q:

Q:

A:

- The EIDL loan can be used for working capital (including fixed debts, payroll, accounts payable and other bills that cannot be paid because of the COVID-19 impact). The loan may not be used for refinancing of long-term debt, expanding facilities, paying dividends or bonuses, or relocation.

- If you are applying for both PPP and EIDL loans, each should be used to cover different expenses.

Q:

Q:

Q:

Q:

Additional Resources:

- Bank of America (BOFA) now accepts online PPP applications. Borrowers must have:

1) a small business lending and checking relationship with BOFA as of February 15, 2020

2) a small business checking account opened no later than February 15, 2020 and no business credit or borrowing relationship with another bank.

Link: https://about.bankofamerica.com/promo/assistance/latest-updates-from-bank-of-america-coronavirus/small-business-assistance - JP Morgan Chase customers who have an existing account since February 15, 2020 can apply online through their website.

Link: https://recovery.chase.com/cares1 - Citi is reaching out to existing Small Business Banking clients through email once they are ready to take applications. Make sure to provide your latest information by clicking on the Notify Me button. Link: https://online.citi.com/US/JRS/pands/detail.do?ID=paycheck-protection-program

Lenders that do not require an existing account

- U.S. Bank has announced that it will be accepting applications for both new and existing customers.

Link: https://www.usbank.com/business-banking/business-lending/sba-loans/paycheck-protection-program.html - Fountainhead is an SBA-approved and licensed non-bank lender and accepts PPP loan applications from any small business customers

Link: https://www.fountainheadcc.com/ppp - United Business Bank serves in California, Colorado, New Mexico, and Washington and accepts loan applications from both new and existing clients.

Link: https://www.unitedbusinessbank.com/

Link: https://www.sba.gov/partners/lenders/microloan-program/list-lenders

Leave a comment