The newer Life Insurance products and policies like Universal Life are not about just a death benefit anymore. They can give the benefits of a financial plan for you, your family or business.

Here are the Last Two of the Four Main Types of Life Insurance

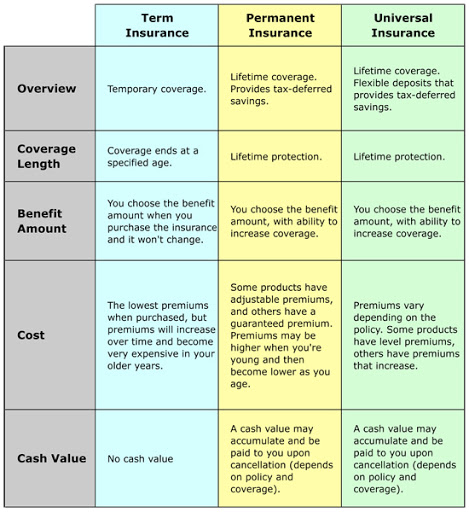

Universal Life Insurance. This type of insurance started in the 1980’s and became more popular with more companies offering it after 2000. This is a type insurance that takes what Whole Life has and maximizes what you can get. ULI has a cash value, usually much greater than traditional Life Insurance as well as many other options. Depending on the terms of the policy, the excess of premium payments made above the cost of insurance is accredited to the cash value of the policy with interest.

With some companies, this is compounded, making much better than most retirement plans because it goes up more and there are no losses!

With ULI, there are also many riders you can get to include living benefits that covers what health insurance does not. Some even pay for retirement homes. It is like having the best of a non-expiring Term Life Insurance policy, that has just a death benefit attached to high interest money market account with tax advantages you do not get anywhere else. In fact, it is so good that many of the upper 1% and most big corporations use these for a tax haven. This is why Wall Street hates them and do not offer them to their clients. Yet, their executives use them for themselves.

Variable Universal Life. Universal Life Insurance can also have a variable investment product. This is basically the same as a Universal Life policy, except that it allocates the cash value into a premium stock market fund. So, the cash value is variable and not predictable. This is good at times when the economy is going well and there are no downturns in the market.

Indexed Universal Life, called the “IUL” in the industry takes the advantages of the Universal Life policy and allocates the cash value into a premium and safe investment such as a stock market index like the Standard & Poor’s 500. This is called the Index Fund Strategy. Because you are in an index fund, typically the best fund to get. In fact, they outperform over 98% of mutual funds and 401 K’s. And if they are secured in a Life Insurance Policy, you are protected against downside loss. So, you get the cash value insurance attached either a fixed account or an equity of a premium index account. You are insured against loss!

Here is what makes this product so good. Your money goes up when the market goes up and your money stays safe and goes not down when the market goes down. This is one of the greatest investment strategies ever created, and only the upper 1% know about it!

Some disadvantages of getting universal life insurance are if the policy is not with a good company or properly structured, then it could include higher premiums, surrender fees, lapse potential and uncertain returns. Very few “retail” life insurance companies and agents really know about them.

If you go to an inexperienced agent or a company that does not have your best interest in mind you may be paying higher premiums, you may not be reminded for a lapse, you may also get uncertain returns and pay too much in fees. So, you can get into a bad deal if you do not know where to go. Allow us to properly help you, we care and listen, and we work for our clients, not a cooperation.

We can help you with this… seminarsonmoney@gmail.com

https://www.policygenius.com/life-insurance/types-of-life-insurance/

https://www.bankrate.com/insurance/life-insurance/permanent-life-insurance/

https://www.investopedia.com/articles/pf/07/life_insurance_rider.asp

Leave a comment